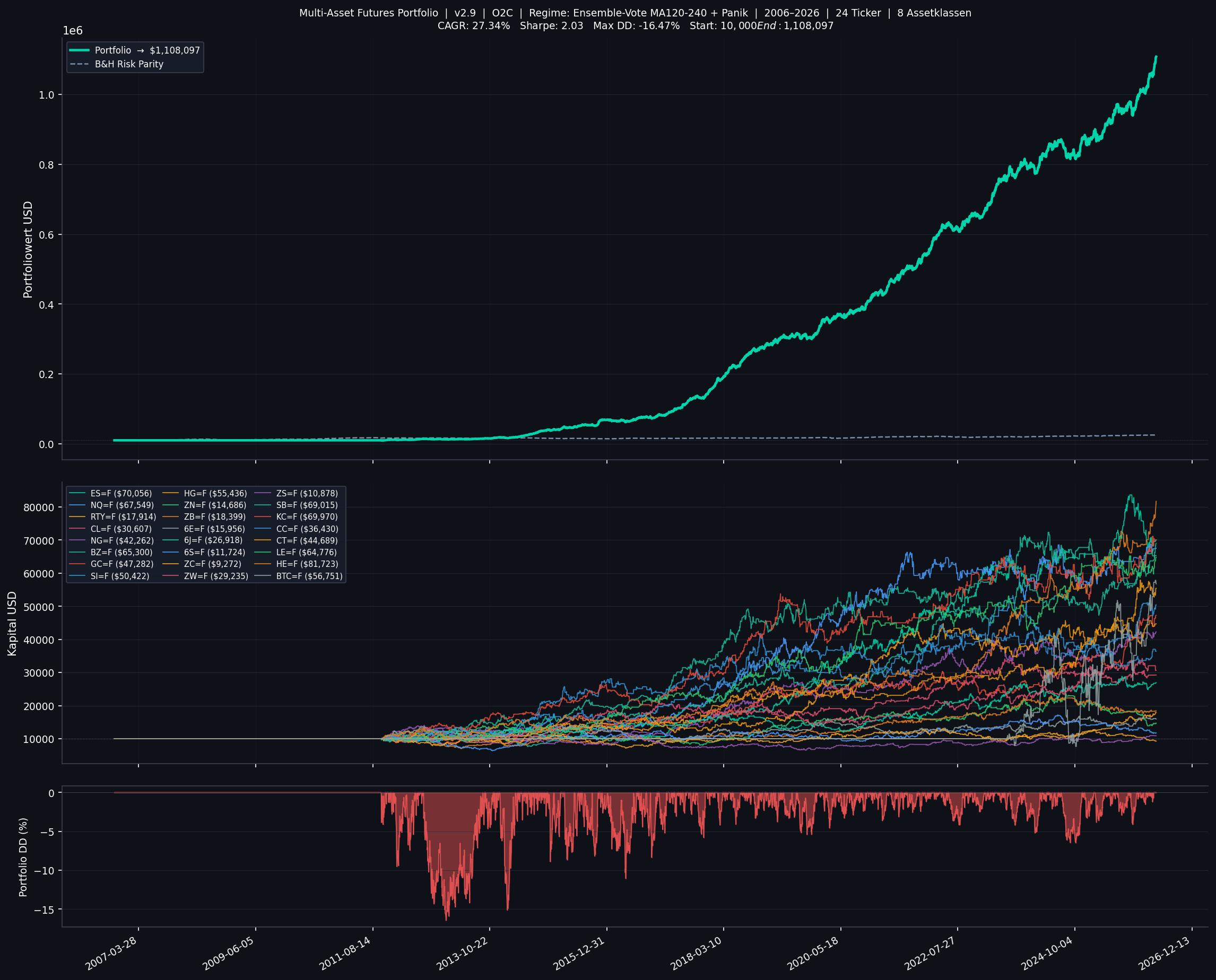

Backtest Performance · 2006 – 2026

20 years. Daily alpha.

12 global futures markets · Benchmark: ES=F

+27.34%

CAGR

2.03

Sharpe Ratio

−16.47%

Max Drawdown

57.5%

Win Rate

1.66

Calmar Ratio

57.5%

Positive Months

Equity Curve

Portfolio vs Benchmark

* Actual backtest results. Past performance is not indicative of future results. All figures are gross of taxes and transaction costs.