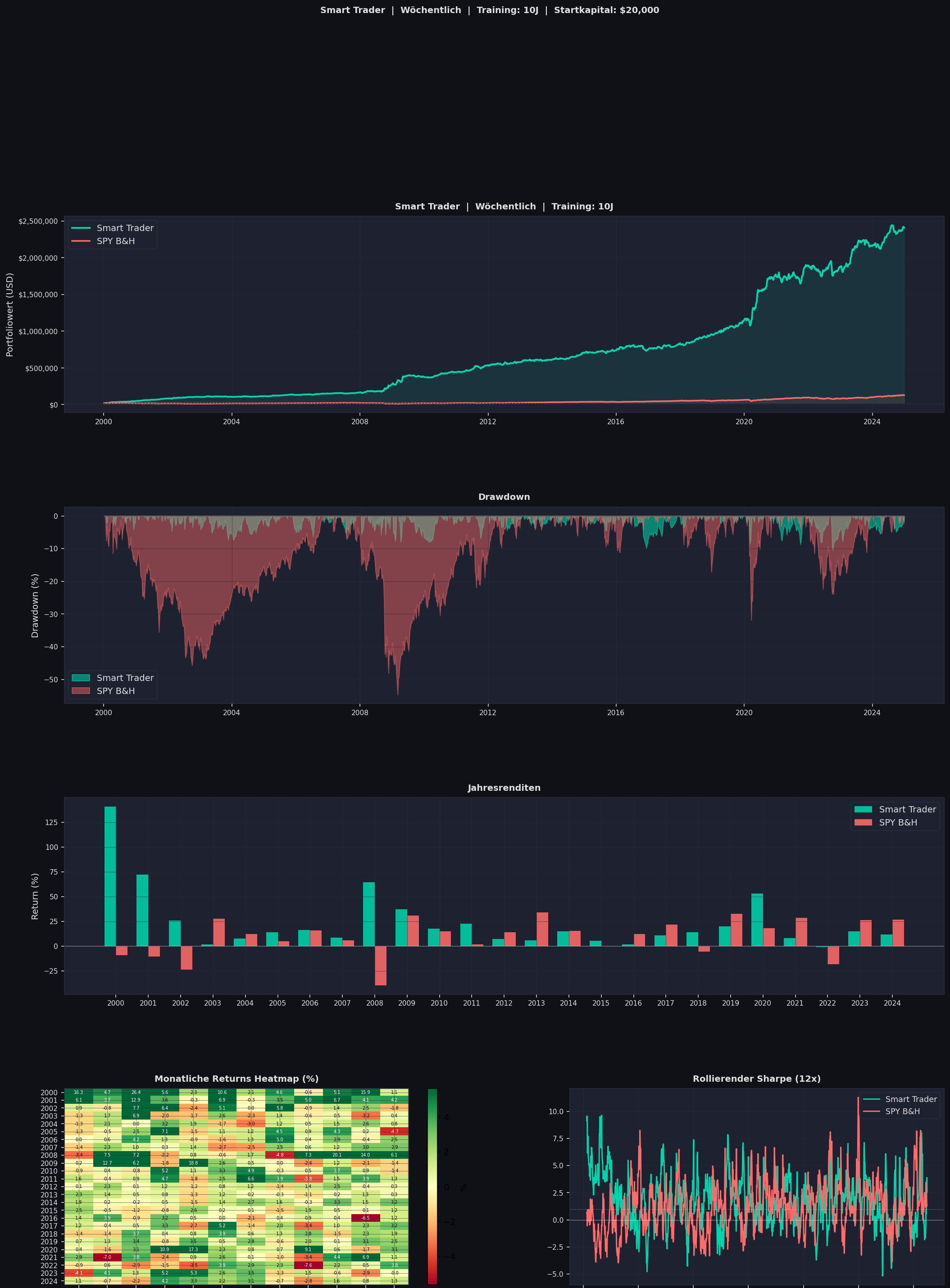

Backtest Performance · 2000 – 2024

25 years. Market-independent returns.

S&P 500 universe · Benchmark: SPY · Weekly rebalancing

+21.07%

CAGR

1.77

Sharpe Ratio

−10.39%

Max Drawdown

+13.38%

Alpha vs SPY

2.03

Calmar Ratio

60.5%

Positive Weeks

Equity Curve

Strategy vs Benchmark

* Actual backtest results. Past performance is not indicative of future results. All figures are gross of taxes and transaction costs.